You taught them how to read and how to ride a bike, but have you taught your children how to manage money?

One study of 2016 college graduates found they carried on average $37,172 in student loan debt. And more than one in ten of them will either default or be delinquent in repaying those loans. 1

For current college kids, it may be too late to avoid learning the hard way. But if you still have children at home, save them (and yourself) some heartache by teaching them the basics of smart money management.

| Tip: Give Them a Look

Find a credit card calculator on the web to give your kids a real-life look at what it actually costs to “buy now, pay later.” |

Have the conversation. Many everyday transactions can lead to discussions about money. At the grocery store, talk with your kids about comparing prices and staying within a budget. At the bank, teach them that the automated teller machine doesn’t just give you money for the asking. Show your kids a credit card statement to help them understand how “swiping the card” actually takes money out of your pocket.

Fast Fact: Pass it On

71% of current college students say they learned money management from their parents.— Source: Sallie Mae, Majoring in Money 2016 |

Let them live it. An allowance program, where payments are tied to chores or household responsibilities, can help teach children the relationship between work and money. Your program might even include incentives or bonuses for exceptional work. Aside from allowances, you could create a budget for clothing or other items you provide. Let your kids decide how and when to spend the allotted money. This may help them learn to balance wants and needs at a young age, when the stakes are not too high.

Teach kids about saving, investing, even retirement planning. To encourage teenagers to save, you might offer a match program, say 25 cents for every dollar they put in a savings account. Once they have saved $1,000, consider helping them open a custodial investment account, then teach them to research performance and ratings online. You might even think about opening an individual retirement account (IRA). With the future of Social Security in question, your kids may be on their own to pay for their retirement. Some parents offer to fund an IRA for their children as long as they are earning a paycheck.2

As you teach your children about money, don’t get discouraged if they don’t take your advice. Mistakes made at this stage in life can leave a lasting impression. Also, resist the temptation to bail them out. We all learn better when we reap the natural consequences of our actions. Your children probably won’t be stellar money managers at first, but what they learn now could pay them back later in life — when it really matters.

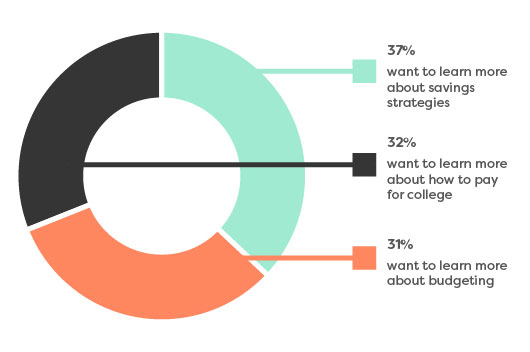

Tell Me About It

More than eight-in-ten college students say they want to learn more about specific aspects of managing money. Of those 80%, here’s what they want to know.:

Our professionals meet with college graduates to guide them on money management. Have your college graduate call us to make an appointment at 315.701.6350, or email [email protected].

1. Forbes, February 21, 2017

2. Contributions to a Traditional IRA may be fully or partially deductible, depending on your individual circumstance. Distributions from traditional IRA and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59 1/2, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70 1/2, you must begin taking required minimum distributions.

|

|

|

Our firm provides the information on this website for general guidance only, and does not constitute the provision of legal advice, tax advice, accounting services, investment advice, or professional consulting of any kind. The information provided herein should not be used as a substitute for consultation with professional tax, accounting, legal, or other competent advisers. Before making any decision or taking any action, you should consult a professional adviser who has been provided with all pertinent facts relevant to your particular situation. Tax articles in this website are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding accuracy-related penalties that may be imposed on the taxpayer. The information is provided “as is,” with no assurance or guarantee of completeness, accuracy, or timeliness of the information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability, and fitness for a particular purpose.

|